How does the bitcoin source code define its 21 million cap?

Many of bitcoin’s staunchest critics have expressed doubt about its 21 million cap, but perhaps the most mindless criticism relates…

,

First published: 10/21/2022

| Last

updated: 01/11/2023

| -- min read

Roth IRAs can be powerful tools, but funding strategies can vary from person to person. To help you take advantage of tax-free bitcoin in a Roth IRA, we’ll cover the four primary ways to get your money in the door—from simply making cash contributions (up to certain limits) to converting an old retirement account. As always, consult a tax advisor to verify your personal tax strategy.

Roth IRAs are becoming an increasingly popular vehicle to hold bitcoin savings. We cover this in-depth in our ultimate guide to bitcoin IRAs, but here’s a quick glance at the benefits of a Roth IRA as it relates to bitcoin:

If your income is below specific IRS-defined caps, you (and your spouse) are allowed to contribute directly into a Roth IRA up to the annual contribution limit. At the time of this writing, limits are up to $6,000 per person, with an additional $1,000 available for those over age 50. This is the most straightforward way to fund an IRA and can be a great way to stack bitcoin savings for the long term.

If your income is below specific IRS-defined caps, you (and your spouse) are allowed to contribute directly into a Roth IRA up to the annual contribution limit. At the time of this writing, limits are up to $6,000 per person, with an additional $1,000 available for those over age 50. This is the most straightforward way to fund an IRA and can be a great way to stack bitcoin savings for the long term.

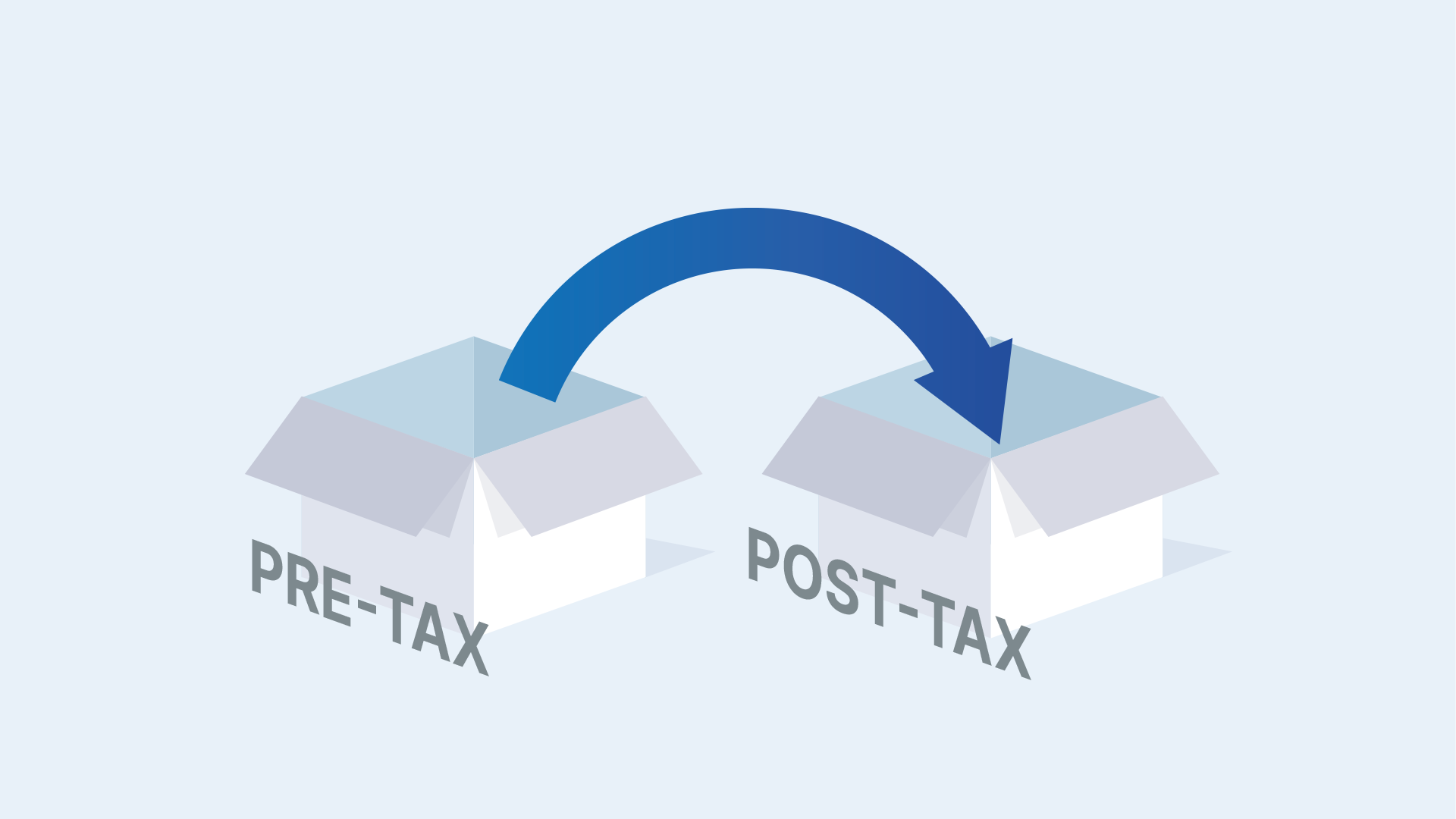

A Roth conversion allows you to convert your pre-tax retirement assets (such as Traditional IRAs, 401(k)s, and other non-Roth employer plans) into post-tax Roth assets—including bitcoin.

A Roth conversion allows you to convert your pre-tax retirement assets (such as Traditional IRAs, 401(k)s, and other non-Roth employer plans) into post-tax Roth assets—including bitcoin.

You have to pay income tax on the converted amounts, but you’ll be eligible to make tax-free withdrawals from the account in the future. You can think of it as “closing your tab” with the IRS. You decide to pay tax now so the bitcoin can be tax-free later.

No income limitations exist when converting a Traditional IRA to a Roth IRA. You can convert any amount during any tax year, but that conversion will count as ordinary income (think climbing tax brackets) in the year performed.

A Roth conversion can be accomplished in several ways, the most common of which include:

The first two methods are the easiest and most efficient. In a 60-day rollover, failure to deposit the money within time will cause the amount to be treated as taxable income (and you may also face a 10% penalty on early distributions if you’re under age 59½).

Roth conversions in a bitcoin world can be powerful due to the inherent volatility of the asset. When the bitcoin price dips, a Roth conversion allows you “close your tab” with the IRS at a cheaper rate, and the ride back up is all tax-free.

For an example of how this works, check out the section on Roth conversions in our article on various strategies for dealing with bitcoin volatility.

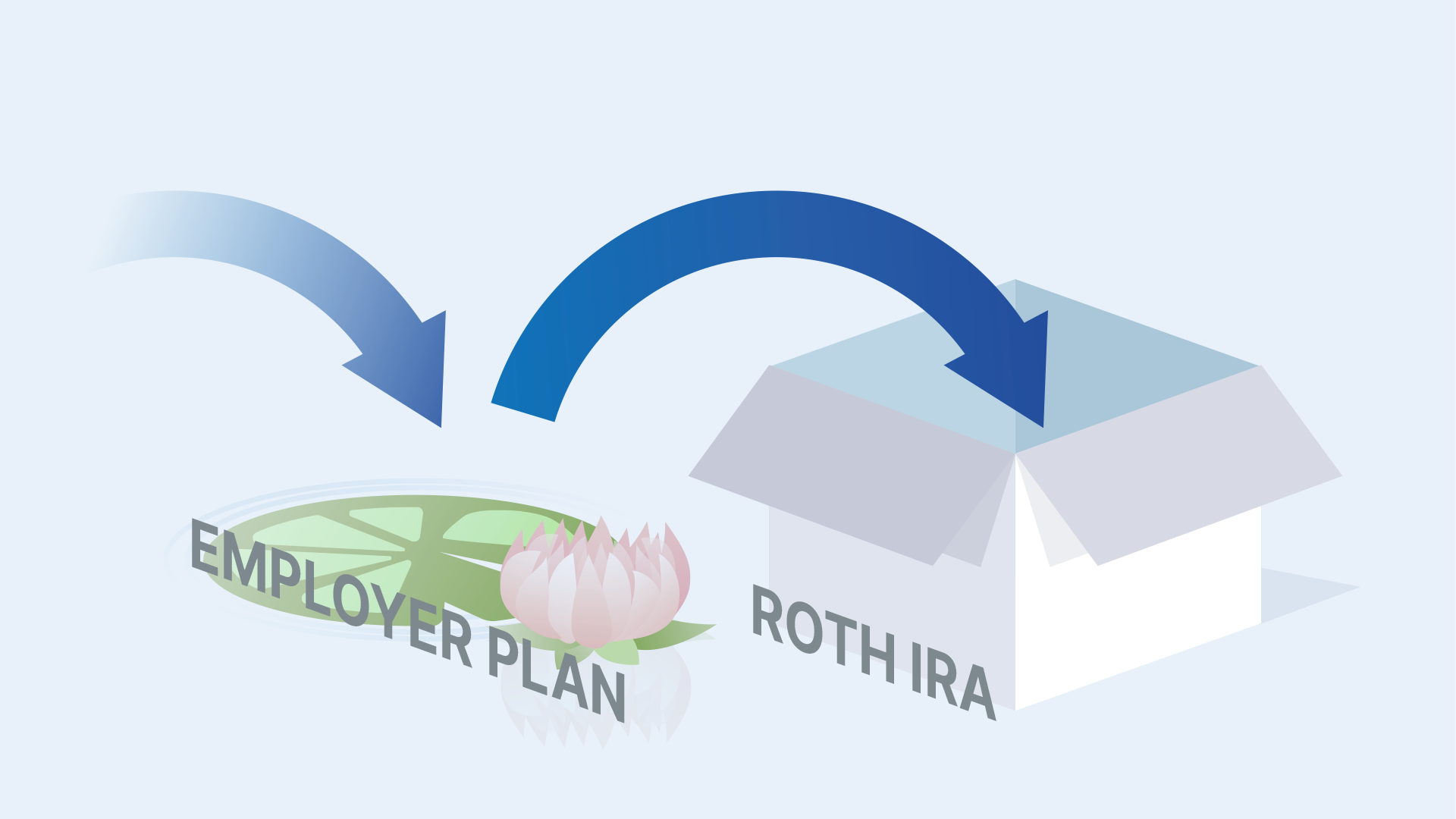

Backdoor Roth contributions are a popular way for high-income individuals to save bitcoin tax-free. A “backdoor” Roth contribution is an informal term for a technique higher-income taxpayers can use to get around the income limits for direct contributions.

Backdoor Roth contributions are a popular way for high-income individuals to save bitcoin tax-free. A “backdoor” Roth contribution is an informal term for a technique higher-income taxpayers can use to get around the income limits for direct contributions.

Since Traditional IRAs have no income limits on eligibility, high-income taxpayers can make non-deductible contributions to Traditional IRAs and subsequently convert those contributions into Roth IRAs. Since the contribution was non-deductible in the first place, there is no extra tax incurred during the conversion. Metaphorically, the contribution hops across a “lilypad Traditional IRA” before landing in Roth. This has the same net effect taxwise as making a standard direct contribution.

To continue the metaphor, if a Traditional IRA is “already occupied” by existing pre-tax assets, hopping across could be more complicated. This is due to the IRA aggregation rule. Effectively, you need a clean slate Traditional IRA to seamlessly transition your non-deductible contribution to Roth.

If you’re interested in making a backdoor contribution to a bitcoin IRA, we have a detailed guide just for you!

The “mega backdoor” contribution is a heftier version of the standard backdoor method (described above). The mega backdoor uses employer plans (predominantly SEP IRAs and Solo 401(k)s) as the pre-tax vehicle to catch the initial contribution before conversion. Employer plans generally have higher limits, allowing you to contribute and convert more than $6,000 per year. The maximum 2022 contribution amount for the mega backdoor strategy is $61,000—nearly three whole bitcoin at this writing!

The “mega backdoor” contribution is a heftier version of the standard backdoor method (described above). The mega backdoor uses employer plans (predominantly SEP IRAs and Solo 401(k)s) as the pre-tax vehicle to catch the initial contribution before conversion. Employer plans generally have higher limits, allowing you to contribute and convert more than $6,000 per year. The maximum 2022 contribution amount for the mega backdoor strategy is $61,000—nearly three whole bitcoin at this writing!

SEP IRAs and Solo 401(k)s are the most viable options for self-employed individuals. Non-self-employed individuals may not be allowed to contribute via mega backdoor since their employer plan must allow for “in-service” rollovers (see 2A above). Again, please consult with your tax advisor to verify strategies that fit your personal situation.

Whether you’re above the income limit and need to perform a backdoor contribution, or you’re just getting started contributing to your bitcoin Roth IRA directly, Unchained is here to help. With any of the above methods, our Unchained Roth IRA lets you save bitcoin on a tax-advantaged basis while holding your keys with multisig. If interested, set up a consultation with one of our experts.

Many of bitcoin’s staunchest critics have expressed doubt about its 21 million cap, but perhaps the most mindless criticism relates…

,When Satoshi Nakamoto created bitcoin, he established in its code a fixed number of bitcoin that will ever exist. Since…

Originally published in Parker’s dedicated Gradually, Then Suddenly publication. Bitcoin is often described as a hedge, or more specifically, a…