Originally published in Parker's dedicated Gradually, Then Suddenly publication.

Bitcoin is often described as a hedge, or more specifically, a hedge against inflation. Chamath Palihapitiya, respected in many circles as a venture investor, once described bitcoin on CNBC as schmuck insurance, qualifying that it’s the single best hedge against the traditional financial infrastructure, “just in case.” Hedging typically refers to hedging risk. An oil producer may hedge by selling an oil commodity future, locking in future revenue at a certain price to avoid the risk of interim price volatility. Inflation hedges, more broadly, are geared toward investments or derivatives that will offset the risk of general price inflation. Historically, these typically include the likes of gold, real estate, commodities, and more recently, stock indexes–anything that would be most expected to “increase” in value as an offset to the dollar decreasing in value. In essence, an inflation hedge is intended to counter the risk and the expectation of the dollar losing its purchasing power.

More generally, individuals and businesses hedge to reduce future uncertainty. An outcome which presents risk might be possible or probable but to varying degrees, the future is inherently unknown. Hedges protect against the potential adverse impact of different future scenarios, which may or may not occur. It is similar to the idea of schmuck insurance in the context that Palihaptiya uses it. There is a generally understood risk that the men and women who manage U.S. fiscal and monetary policy might screw up the dollar economy, materially or completely. In this scenario, there is an argument to be made that bitcoin has at least a chance to be an alternative financial system, which could be viewed as “insurance” should the schmucks create a mess. Regardless of the cause or degree, the dollar is expected to lose purchasing power, and it presents risk worth hedging. In a worst case scenario, the dollar could be broken beyond repair, and bitcoin offers the promise of a currency system with a fixed supply. Realistically, it should meet the classical definition of either an inflation hedge or schmuck insurance as both are most commonly understood.

While it may meet the classical definition, any view of bitcoin as a hedge or as insurance, in the traditional sense, misses the most fundamental aspect of bitcoin on a wholesale basis. Bitcoin is not a hedge against inflation; it is the permanent solution to inflation, and those are two very different things. Bitcoin might be volatile, but over a long time horizon, it is not a risk. Risk and volatility are commonly conflated but in reality, are similarly very different. Volatility can present a risk depending on time horizon, but it is not inherently the same as risk. Risk speaks to future uncertainty, and hedges against risk intend to reduce future uncertainty. Bitcoin may not be widely or well understood yet, but it is more knowable than it is uncertain. The gap is one of knowledge rather than risk.

The Fundamental Value of Bitcoin

All value in bitcoin derives from the fact that there will only ever be 21 million, and it is possible to know, or to form an understanding as to, how bitcoin enforces its fixed supply and whether it is credible. That is knowable, and it is the most fundamental basis to explain how and why bitcoin is competing with the dollar as money. Every inflation hedge is intended to earn more dollars or appreciate in dollar terms to offset inflation, whereas bitcoin is structurally designed as a replacement, which is a critical distinction. Competition may signal chance or uncertainty, but there is objectivity and empirical evidence (14 years / 770,349 blocks) to inform the outcome.

If A, then B. If bitcoin credibly enforces its fixed supply of 21 million, then it will replace the dollar (euro, yen, pound, peso, etc.) as the currency which facilitates practically all day-to-day commerce in each respective local economy (see Bitcoin Obsoletes All Other Money). If A is knowable, then B is knowable. Just because any particular individual might not know “A” and might not understand the causal relationship to “B,” that does not make the equation unknowable.

In the dollar world, inflation is a man-made phenomenon. Most simply, new money is created by the Federal Reserve and each unit purchases less in the future as a result. In mainstream economic circles and high finance, there are many prevailing theories as to what causes price inflation but look no further than the supply of dollars. What principally confuses people is how the increase in the supply of dollars is transmitted through the economy, and specifically, to the dollar price of real goods and services. This is one place where common sense prevails. If more dollars are created, each dollar will purchase less because the creation of more dollars cannot and does not increase the supply of real goods and services available in the economy.

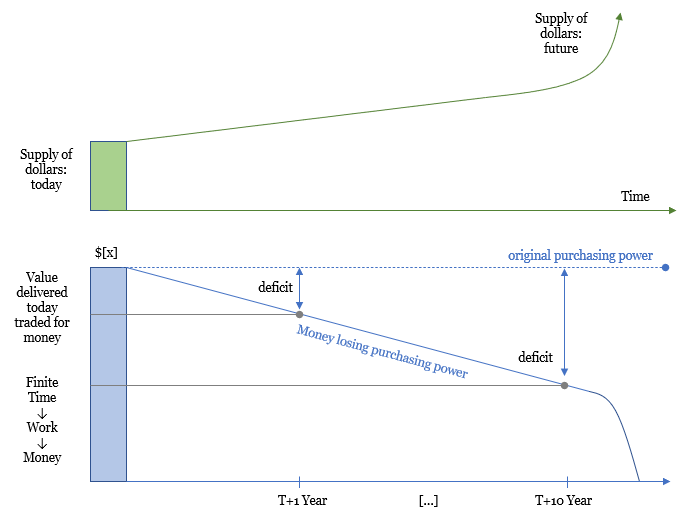

Human time, at an individual level, is finite, but the supply of money is not. The Federal Reserve has flooded the market with trillions of dollars since the great financial crisis–$8 trillion to be specific– which has increased the dollars in circulation by ~10x. Dollars are becoming more and more abundant, and as the money supply increases, the purchasing power of each dollar declines. When money loses its purchasing power, it is the equivalent of an hour of work being guaranteed to purchase less than the value actually delivered in the past.

All else being equal, it amounts to a barrel of oil produced today purchasing less than a barrel of oil in the future. The incentive structure breaks entirely when money is created at no cost, and the problem is not static. As more time passes and more money is created, the purchasing power of value delivered at various points in the past degrades further and further, until it eventually purchases nothing of comparable value (or time to produce). In substance, it results in people having delivered value in the past and never having the value returned.

To use an extreme for illustrative purposes, imagine you spent 40 hours in a week working for $10 per hour ($400 total). Then consider the consequence if the dollar’s value were to “hyperinflate,” effectively trending to zero over a short period. That would translate to a week of time which you can never get back and which would purchase you nothing in the future. In the practical application of hyperinflation, it is not just a week that is lost but instead, entire life savings. It is a path to sure ruin, but really, anything on the spectrum of currency devaluation is similarly problematic. Time is required to produce work, which translates to goods and services. Any time expended in the past saved in a form of money which purchases less in the future creates a deficit. As dollars become massively more abundant and time remains finite (past, present and future), more dollars compete for a relatively fixed quantity of goods and services. People value each dollar less and charge more dollars for each unit of their time in an attempt to reduce the deficit created by more money having been created and to offset the expectation of future degradation. More dollars, same amount of time. Inflation is that simple but the consequence is not.

The mistake most people make, especially academics, is believing it can go on forever. Just print a little bit of money, or even a lot, and things (i.e. goods and services) will merely cost more dollars. What’s the big deal? The Fed has been doing this for decades, nearly a century. If money were as simple as basic math, it might be the case. But in reality, the function of money is highly complex and consequential. Money coordinates practically all economic activity, functionally by facilitating trade between every person for all goods and services. The creation of money, especially at little to no cost, does not just cause the value of the currency to depreciate; it fundamentally impairs that currency’s ability to coordinate economic activity. Hyperinflation does not occur simply because too much money was printed, in an arithmetic sense. Instead, it is the distortion of the money which actually makes trade more difficult and which causes imbalances that ultimately lead to supply chains breaking down. Yes, the currency becomes more abundant, but the basic goods necessary for survival, like the delivery of energy, become more scarce at the same time as the incentive structure of the money becomes increasingly fractured. In each instance of hyperinflation, history has shown this to be true. The currency fails completely because of the breakdown in trade, the principal function which money helps to facilitate and coordinate.

The incremental error would be to believe or hope there is something different in the case of the dollar. There is no “better” when it comes to massively debasing a currency; the function by which the currency breaks down, to the point of not functioning, is all the same. Avoiding the reason and logic does not change any future reality. It is predictable and knowable, albeit a bit uncomfortable. But human beings are collectively intelligent, adaptable and resilient, which is core to survival and progress. Dealing within reality is not dystopian; it is just reality and those that thrive through adversity are the ones that best adapt. And, it is also why bitcoin is such a great source of optimism and hope for those who do adapt. Bitcoin provides a light at the end of the tunnel, a solution to the ultimate problem. If not for a solution in hand, it might be very reasonable to be pessimistic about the future. Thankfully, the world has already adapted to create a solution to the broken structure of the dollar. Most people just don’t know it yet. If the problem is the printing of money, then the antidote is a form of money that cannot be printed, which is what bitcoin represents. There will only ever be 21 million bitcoin and that is the fundamental value of bitcoin.

The Complexity of the Dollar System & Inflation

Even still, the question does remain. Why has the purchasing power of bitcoin declined, more recently, relative to the dollar–if more dollars are being created, if dollar inflation is increasing, if bitcoin does have a fixed supply, and if all of the prior logic were to be true? This is the most common question I have heard over the past twelve months. The skeptic will exclaim, “but I thought bitcoin was supposed to be a hedge to inflation and there is inflation. What gives?” That’s the thing, it’s not a hedge. People cannot flee to any good, but especially not to bitcoin, for “safety” without prior understanding or knowledge. Few people have a deep understanding of bitcoin and even fewer the dollar but more people rely on the dollar today, than bitcoin. That is the unavoidable state of the world and the dollar system is in the critical path to understanding how facts which otherwise might seem to contradict each other are actually perfectly consistent.

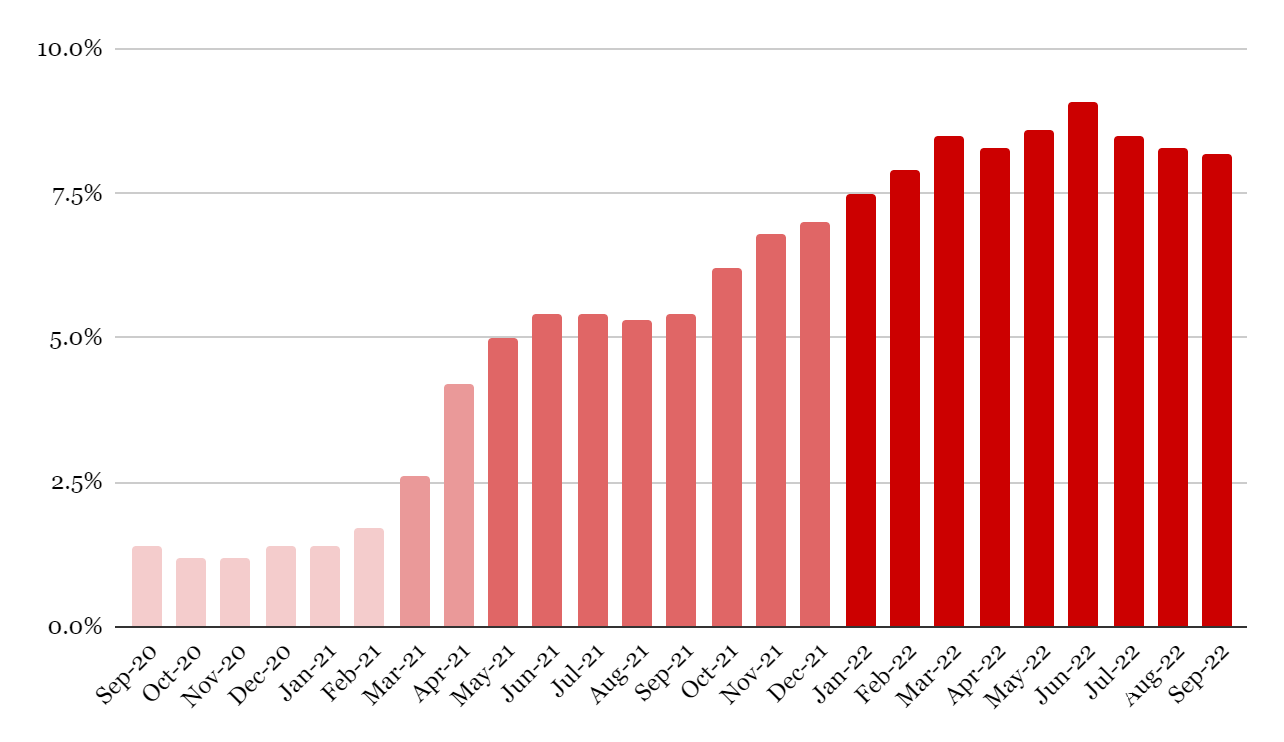

There is material dollar inflation in goods and services, yet the dollar’s value has been appreciating relative to virtually every other asset as well as all other currencies, including bitcoin, over the past year. What explains this reality? Because something must, and it is not merely a coincidence. The Consumer Price Index (“CPI”) measure of inflation in the U.S., the most commonly used benchmark, started to accelerate in the first half of 2021, and year-over-year, CPI inflation has exceeded 7.5% in each of the past eight months. Looking back two years, price levels in September 2022 were 14.0% higher compared to September 2020, which is approximately how much less the dollar in your bank account can purchase today versus just 24 months ago.

U.S. CPI Inflation (Y-o-Y Change)

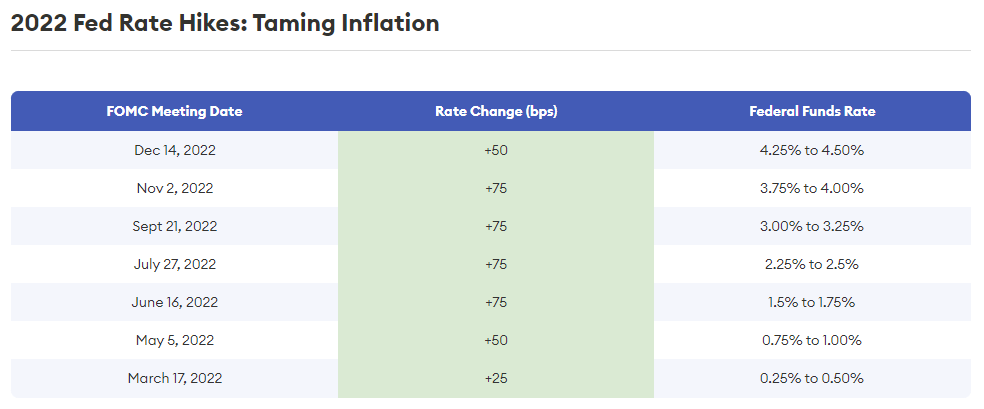

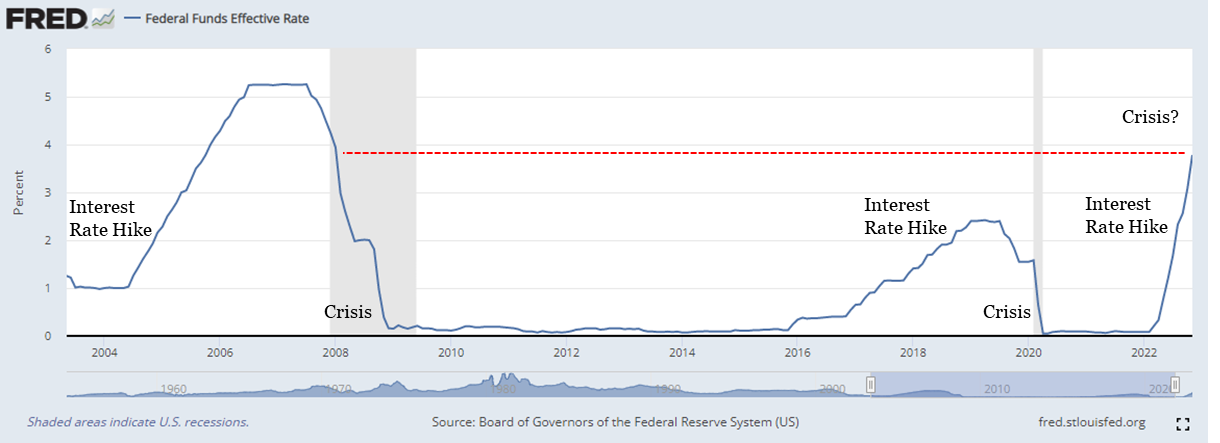

In response to this acceleration, the Federal Reserve signaled to the market that it would pursue a concerted effort to reduce inflation in the Fall of 2021, and it ultimately began to raise interest rates (from zero), as a means to that end, in March 2022. Cumulatively, the Fed raised interest rates seven individual times in 2022 to the tune of 4.25% in total rate increases, with a current targeted Fed Funds rate (the rate off of which virtually all other market interest rates are set) between 4.25% and 4.50%. At these levels, the current Fed Funds effective rate is higher than any level dating back to just before the financial crisis in early 2008.

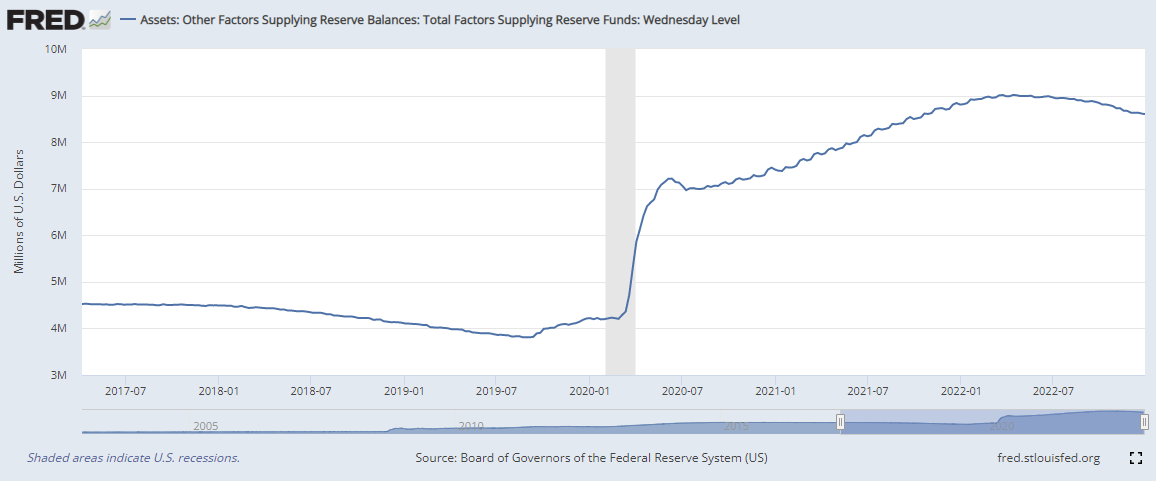

About a year prior to the initial acceleration in inflation, the Federal Reserve took “emergency” measures to massively increase the supply of dollars in the financial system. From September 2019 to September 2021, the Fed increased the money supply by $4.7 trillion, more than doubling the amount of dollars in circulation. It was a near redux of the Great Financial Crisis. In September 2019, a large overnight funding market, commonly known as the Repo market, experienced significant instability and market interest rates tripled. Not coincidentally, this occurred as the Fed was actually in the process of gradually reducing the supply of dollars. Contagion spread and instability became more acute as the global economy was soon thereafter shut down, which resulted in an even more drastic increase in the amount of money that was created. The inflation currently present and which began to accelerate in early 2021 all ties back to the cumulative increase in the supply of dollars, over the past few years and decades.

Supply of Dollars: Base Money (2017-2022, $ in trillions)

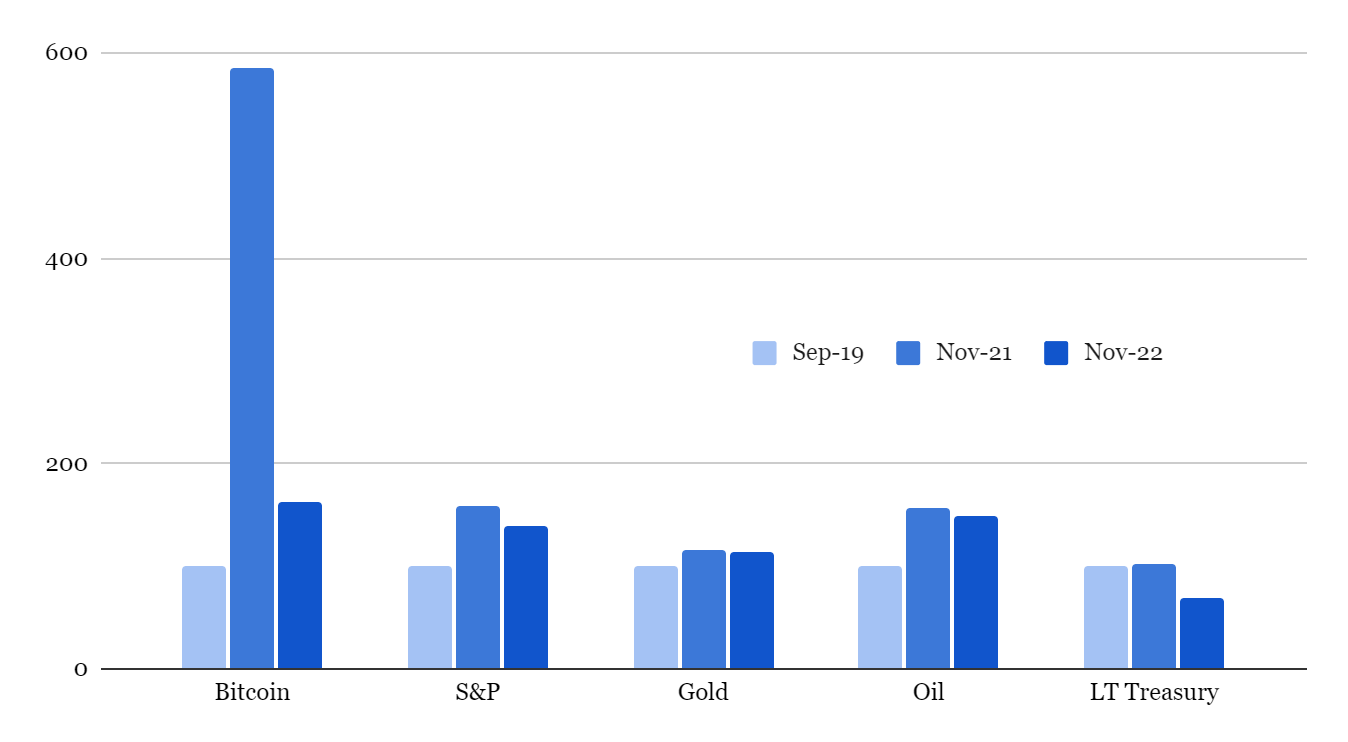

This is the Fed’s system. Print money, cause inflation; raise interest rates, cause financial instability, and repeat. The aggressive increase in the supply of money followed by aggressive increases in interest rates and vice versa creates economic chaos. Asset prices today in dollar terms indexed to the price levels prior to the most recent epoch of money printing (September 2019) demonstrate a cumulative devaluation of the dollar, which is consistent with the trend of CPI inflation of goods and services. Compared to September 2019, each bitcoin, the S&P 500, gold and oil are all more expensive today in dollar terms, with long-term treasury bonds actually losing purchasing power and bitcoin outperforming each of the others.

However, if you isolate for the period after which the Fed began to signal interest rate increases–approximately the last twelve months–to tame inflation, all asset prices have declined relative to the dollar, despite goods inflation remaining elevated. Bitcoin has outperformed each of the other benchmark assets on a cumulative basis, but it has also had the largest correction from a year ago. Undoubtedly, the failures of many counterparties which trade bitcoin have impacted the extent of bitcoin’s correction, but the driving force behind the more fundamental shift in asset price levels, for which bitcoin is not immune, has everything to do with the shift in the Fed’s monetary policy–the marginal increase in interest rates and decrease in the supply of dollars.

Asset Prices Indexed to September 2019 (2019 = 100)

While bitcoin is material in size (~$350 billion in purchasing power today), it remains small relative to global financial assets which are estimated between $300 trillion to $400 trillion. For context, the S&P 500 has a current market capitalization of $30 trillion and while it might have “only” declined by 11.5% over the past twelve months, that decline equates to nearly $4 trillion in paper wealth that has disappeared, which is over 10x the present total purchasing power of bitcoin. Comparatively, total debt system-wide in the U.S. is $92 trillion, with Federal government debt alone standing in excess of $26 trillion. The market value of bonds in the U.S. has similarly declined by multiple trillions over the past twelve months. In short, nothing is immune to the dollar so long as it is the 800-lb gorilla, and scale matters, especially when considering volatility.

The dollar economy is the largest financial system in the world, by a wide margin. There is no getting around that the dollar is the primary global funding currency, and it remains the currency which facilitates by far the most global commerce. As goes the dollar, so goes the world. Or rather, as goes the Federal Reserve, so goes the world (at least today). Massive shifts by the Fed in managing U.S. monetary policy impact all assets, not just bitcoin. When the Fed reduces the supply of dollars and increases interest rates, all asset prices become pressured. Liquid assets typically get sold first (easiest to sell) to source dollars in an attempt to shore up balance sheets and to fund future obligations on dollar-denominated debt liabilities. Over the short-term, bitcoin might be disproportionately impacted due to its relative size and its nascency, which contribute to volatility (up and down) but every asset traded for dollars is impacted.

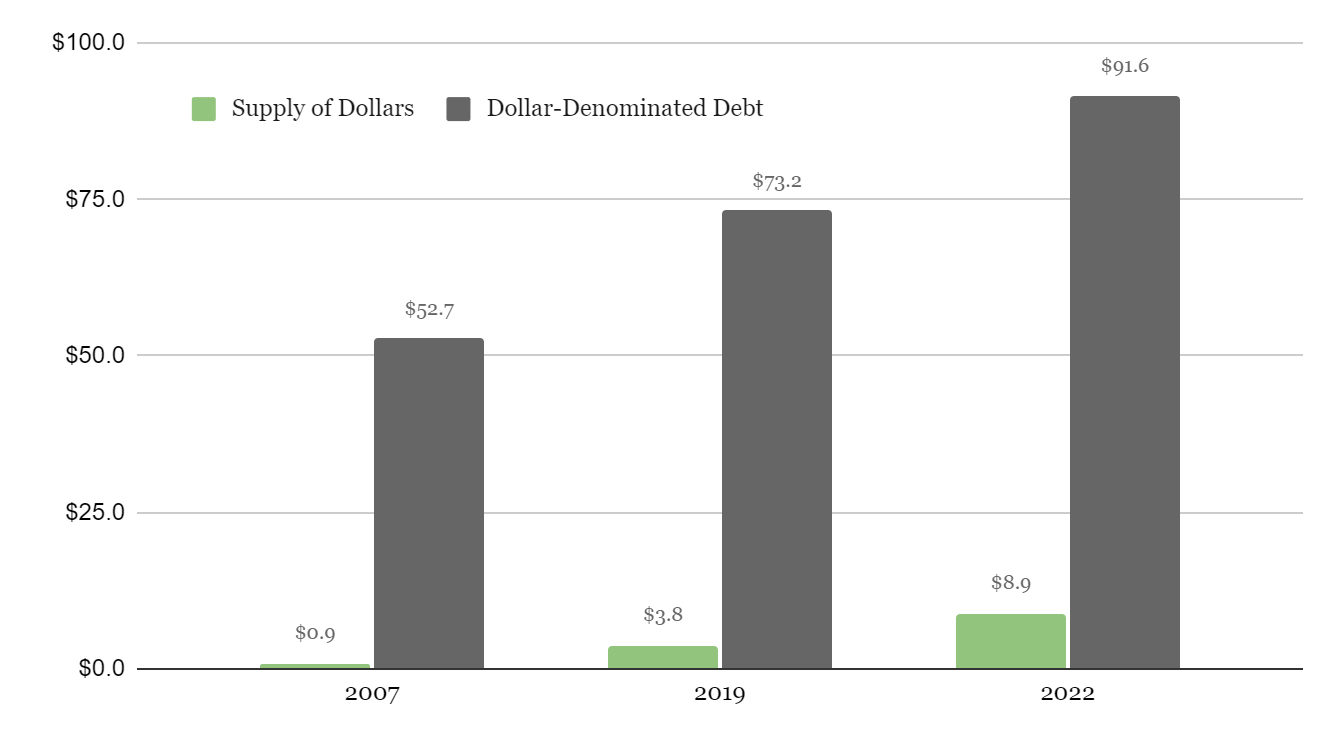

Supply of Dollars vs. Dollar-Denominated Debt ($ in trillions)

This chart best explains everything that matters in regard to the dollar and its machinations. Why inflation does not simply mirror the increase in supply of dollars. Why bitcoin can intermittently decline in purchasing power despite all the cumulative money printing (and goods inflation). Why it is (and has always been) a certainty that the supply of dollars will increase drastically from any point in time. And importantly, why bitcoin will replace the dollar.

Today, there is approximately $92 trillion in dollar-denominated debt in the U.S. credit system but there are “only” $9 trillion actual dollars. Despite the money supply having increased by nearly 10x since before the financial crisis, there remains over $10 of dollar-denominated debt for every dollar that exists today. Only dollars can pay dollar-denominated debt and in this context, dollar debt only includes the most vanilla of anything that could be considered debt; bonafide fixed maturity, fixed liability debt as estimated and reported by the Fed. Mortgages, credit card, student loan, auto loan, bank debt, corporate bonds and federal, state and local government debt, etc. It does not include estimates of unfunded pension liabilities or derivatives of debt–merely a fixed amount of dollars owed at a defined future point in time. The Fed may have massively increased the supply of dollars, but the world is still short dollars, dollars which are owed and must be demanded in the future to repay existing debt obligations.

There is too much debt (dollars owed in the future) relative to dollars that actually exist. When the Fed shifts its monetary policy as it did over the past year, to raise the cost of dollar-denominated debt and to reduce the supply of dollars, the market begins to figure out the unavoidable arithmetical fact that the system is far more than just a few dollars short. The market as a whole begins to scramble for dollars–selling assets, raising prices, reducing expenses, raising more debt even at higher cost. Every possible avenue is pursued. Not all debts are due tomorrow, far from it, and not everyone is in debt; but as a whole, the market as a whole is heavily indebted, to the tune of 10:1 and as dollar-financing conditions tighten, the instinct to source and save more dollars to fund future obligations is overwhelmingly one way. It all happens at the same relative time because it is actually caused by the Fed’s actions as an input, reducing the supply of dollars and increasing the cost to refinance dollar-denominated liabilities.

Fed Funds Effective Rate (2004 to 2022)

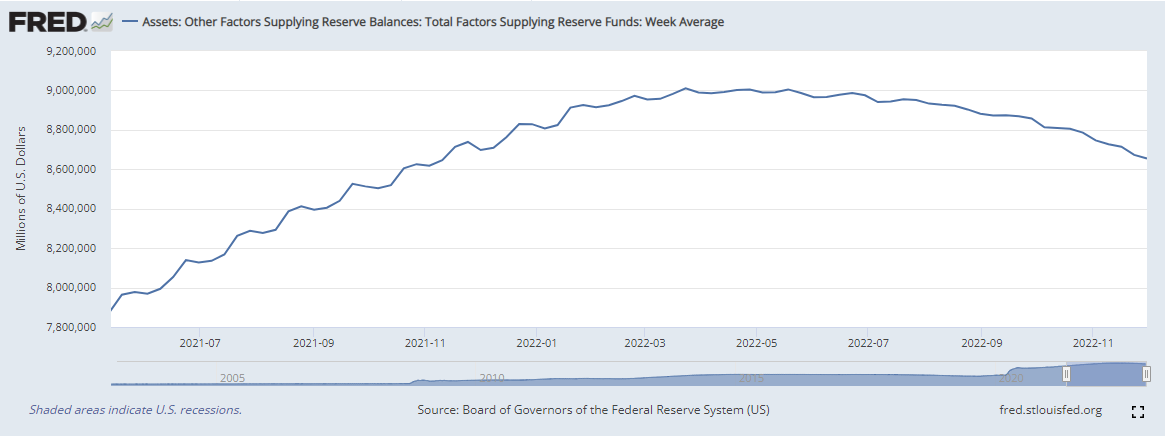

Supply of Dollars: Base Money (2021-2022)

When the Fed reduces the supply of dollars and increases interest rates, the amount of debt in the system does not magically change; recall the $92 trillion in dollar-denominated debt. Instead, there are just fewer dollars to repay the outstanding debts and it becomes more expensive to sustain existing debt levels. Necessarily, not all debts can be repaid. Now, given the embedded degree of system leverage, that is actually always the case regardless of what the Fed ever does next, but the market, individually and collectively just figures out that the magnitude of the problem is far larger and the timing more present, as interest rates rise and as the supply of dollars is actively reduced. The Fed may have begun signaling its plans just over a year ago. But, it did not actually start increasing interest rates until March 2022, and it did not begin to reduce the supply of dollars until June 2022. Somewhere therein is when the time bomb really started ticking.

As a matter of record, the Fed has been more aggressive in raising interest rates in 2022 than any time post the Great Financial Crisis of 2008, and it has withdrawn approximately $350 billion in dollars from the financial system relative to its most recent height, over the past six months. While that may only be ~3.5% of all dollars, it’s still a massive amount of dollars on an absolute basis, and it represents marginal dollars that are no longer available to fund liabilities. The credit system today is also ~75% larger than it was in 2008. Because every dollar is leveraged 10:1, the reduction in the supply of dollars has an outsized impact on the financial system as a whole. But also remember that the system was already far more than a dollar short. The directional shift does matter but maybe most consequentially, because it wakes the world up to a larger problem that already existed and is actively being magnified. It might seem simple, but that is the point. Everything happening–each significant economic shift–can be explained by the amount of dollars that exist, the amount of debt that exists, the change in supply of dollars and the change in the cost to finance debt.

The existence of a debt (or credit) system that is an order of magnitude larger than the amount of money that actually exists causes a few dynamics that may not be immediately intuitive. When the Fed digitally creates money, there is still far more debt that exists, which is what prevents the dollar from immediately collapsing in value. In the end, the existence of more dollars does cause each dollar to purchase less in the future (and over time) but the credit system, given its size, is necessarily at the crux of how it all plays out. The debt-to-dollar dilemma is what anchors the dollar’s value on a near term basis. The liabilities are fixed in the sense that a fixed amount of dollars are owed.

These liabilities create high present demand for dollars, and the liabilities have claims on real assets such as cars, homes, real estate developments or equity in productive companies, etc. For example, if you owed $10,000 on your car and could not repay the debt, not only would you do everything you could to source dollars; but, the effective price of your car is anchored to the amount of debt owed to the bank in order to satisfy its claim. It does not matter how many dollars have been created, that claim is real, and more broadly, fixed debt liabilities functionally set the price of existing assets in a system in which debt claims massively exceed the supply of dollars (and especially, when it becomes apparent that debts cannot be repaid).

At the same time, the system leverage is also what guarantees that the Fed will have to print more dollars in the future. If it did not, the credit system would collapse entirely. The introduction of more dollars in a time of financial crisis or instability is really designed to prevent the credit system from collapsing. The Fed responds to the need for more dollars to service debt-denominated liabilities by supplying more dollars. This is what occurred in 2008, it’s what occurred in 2020 and it is what will occur again and again. First, the existence of more dollars allows existing debt levels to be sustained, but then with more dollars floating around, more debt can actually be created. Note that the Fed has increased the supply of dollars by approximately $8 trillion since 2007, but the amount of dollar-denominated debt has increased by $39 trillion over the same period. On a percentage or multiples basis, the amount of dollars has increased by significantly more but on an absolute basis, the increase in the amount of debt has dwarfed the increase in the supply of dollars. For every dollar that has been printed, more debt has been created.

Again, scale and size matter, particularly for the reason that only dollars can repay dollar-denominated debt. On a relative basis, yes more dollars exist, but there are far more liabilities that need to be funded. Each dollar purchases less over time for the reason that there are more, but at any point that dollars begin to be removed, a real problem exists, especially for those short dollars. However, because the system as a whole is functionally insolvent, everyone is impacted–not just those in debt. There is no escaping it; all asset prices are impacted and everything becomes increasingly volatile when a run on the remaining liquidity in the financial system occurs. It singularly best explains the phenomenon of everything around you that you need day-to-day costing more in dollars, while observing asset prices, including bitcoin, your home or the stock market, moving in the opposite direction.

The goods most needed day-to-day for survival (food, water, gas, power, etc.) do not become any more abundant or any easier to produce as a result of money being created or money being removed from the financial system. While there is arithmetic consequence to the problem of funding dollar-denominated debt with dollars, the economic engine is massively complex. The U.S. economy is comprised of hundreds of millions of people, connected to supply chains of billions of people, each who have a combination of skills or jobs necessary to deliver very basic goods to market and each whose time is finitely scarce, all coordinating their economic activity with dollars. At the end of the day, near term inflation of goods and services as well as the intermittent change in asset price levels is explained by the changes in the money supply, but focusing on the month-to-month or year-to-year change in any price level would fail to see the forest through the trees. It is the surface level, first derivative impact; any focus on the short-term (a year, two or even decade) necessarily fails to recognize the more fundamental consequence to a highly complex system.

The manipulation of the money supply distorts economic activity; it distorts the ability for humans to trade. Humans respond to price signals and as those signals become more volatile and less reliable, the basic function of the currency to coordinate trade breaks down. The marginal goods you need, tomorrow and the next day, become more valuable relative to everything else, including money, but also relative to other assets you own like a home or a second home, a car or second car, and especially, any financial asset like a stock or a bond. It is the distinction between assets that have already been produced versus those goods that need to be produced and procured day-to-day to sustain oneself.

The goods necessary day-to-day become harder to produce as the economic engine breaks down, as trade becomes harder to coordinate, and the problems become magnified in a highly leveraged and centralized system. Imagine the complexity of an economic system with hundreds of millions of workers, producing goods and services every day, and then contemplate one in which mass defaults could occur because debt cannot be repaid and whether those issues might be exacerbated by a central bank massively increasing and decreasing the money supply, in a persistent but unpredictable cadence. In practice, money becomes abundant, credit becomes good for nothing and goods become scarce.

Bitcoin is the Solution to Inflation

The Fed’s monetary system appears at first to be a vicious cycle, something that will just always exist and never end. A rollercoaster that someone else put you on but that you can’t get off. The cycles of creating money, persistent inflation and every few years, a financial crisis. Everything becomes more expensive, while everything else feels more out of reach, waiting for the next shoe to drop. The cumulative feeling might best be described as a combination of exhausting and suffocating, particularly at a time when the world seems to be more volatile and the future more uncertain than ever. The matters are made worse when the cause and effect cannot be explained; without prior understanding, it puts people in a position of not knowing what actions to take, when it will end or if it will end. Without explanation and without a solution to the problem, it might be very reasonable to assume the vicious cycle will never end.

Bitcoin simultaneously being the ultimate solution to the dollar and it not being immune to the dollar is entirely consistent with the nature of the problem. An understanding of one, and its challenges, necessarily informs the other as a better alternative and how it may be adopted. Bitcoin is competing with the dollar to replace it as the form of money which coordinates trade and commerce. If one were to accept that there were fundamental problems inherent to the dollar but that it still coordinates practically all economic activity for those that use it, it would stand to reason that any replacement to the dollar would not be immune to its issues during the transitionary period. In an academic world, maybe everyone figures it out at the same time and makes a conscious decision to scrap the old world, adopt the new world, and move on without any consequence to the sins of the past. The dilemma is that money coordinates trade, and trade means the physical manufacture and delivery of goods and services in the real world, which is far more complex than professional economists and academia might suggest.

The world cannot drop a bad money and adopt a better one, like a single individual can drop a bad habit. It’s just not that simple, and that’s ok. Today, the dollar still exists and bitcoin has a total purchasing power of approximately 0.4% of the U.S. credit system, which itself is a fraction – albeit a large one – of the global financial system. If the Fed reduces the supply of dollars and increases interest rates, the purchasing power of bitcoin will reasonably decline on an interim basis relative to the dollar, because the entire world still relies on the dollar, including everyone in the dollar economy who has begun adopting bitcoin. Bitcoin remains relatively small. It is also liquid, and there are very few bitcoin-denominated debt liabilities (on a relative and absolute basis), which means it can be easily sold to source dollars as the supply becomes constrained. In short, dollar inflation can exist and the purchasing power of bitcoin can decline at the same time while the fundamental remains unchanged–that bitcoin is replacing the dollar as a better form of money to coordinate trade.

Bitcoin has fundamental value because of its fixed supply. That is the value proposition: a fixed supply of bitcoin vs. an ever-increasing supply of dollars. In 2007, there were $0.9 trillion dollars estimated in circulation. In 2019, this number was estimated by the Fed to be $3.8 trillion, just prior to the most recent monetary expansion. Today, the estimate is $8.9 trillion. Dollars are created by the Fed and even more dollars will be created in the future as a necessity to fund all the debt that has accumulated in the U.S. credit system. In 2007, zero bitcoin existed because bitcoin did not exist. Bitcoin was launched in 2009, in large part, to solve this specific problem. By 2019, 17.9 million bitcoin were in circulation. Today, 19.2 million bitcoin are in circulation. The remaining 1.8 million will enter circulation between now and approximately 2138 (the next 115 years). There will only ever be 21 million bitcoin, and that is bitcoin’s true innovation.

Whenever something happens in the world, and specifically anything that causes volatility in the price of bitcoin, I always ask myself, “did [x] change anything about the bitcoin network’s ability to credibly enforce its fixed supply?” Now, one might need to know how bitcoin enforces its fixed supply (and its relevance) in order to then evaluate the relative impact of anything to bitcoin. But, that is to the point. Without a prior understanding of how bitcoin enforces its fixed supply or why it’s important, it would leave anyone in a precarious position to evaluate any current event (or its impact) on bitcoin’s fundamental value. Anyone who claims that bitcoin will fail due to the failures of a few private companies almost certainly does not understand how bitcoin enforces its fixed supply or its consequences. Separately, anyone who claims that bitcoin is failing on its promise as a hedge to inflation, similarly could not tell you how bitcoin enforces its fixed supply. Ask anyone who claims bitcoin will fail, or otherwise has failed, that rhetorical question–but, how does bitcoin credibly enforce its fixed supply without the need for trust?

A fixed supply is the principal contrast bitcoin provides to all other forms of money. Bitcoin is trustless, compared to the dollar being a trust-based system, and bitcoin is permissionless, while the dollar is largely a permissioned system. There are other contrasts, but the supply of the currency is the most fundamental. Bitcoin as a trustless and permissionless monetary network would be of little to no value if not for those same properties being necessary to ensure and enforce a fixed supply. But similarly, as a system, bitcoin would not be trustless or permissionless if the currency native to the network were not fixed in supply. The entire value function revolves around the enforcement of a fixed supply; that is what aligns all other economic incentives and allows the aggregate operation to function. The fixed supply is the thing of value to the entire world. In that sense, it is not just what aligns all incentives. It is what creates the incentive. It is why bitcoin exists.

How bitcoin enforces its fixed supply is the innovation and at a fundamental level, the most important technical question to understand. In fact, it is a necessary input to have a true bottom up perspective, not relying on anyone else’s word, and it is specifically the subject of Bitcoin, Not Blockchain and Bitcoin is Not Backed by Nothing. However, first understanding why it is relevant is more sequentially important because it informs how it is possible. It might seem circular but it is not. Any person would necessarily need to understand why a currency that cannot be printed is of value to the world on an individual level, before then understanding the incentives of the network and the mechanisms that enforce the fixed supply.

For example, the statement that bitcoin is the solution to inflation. Why would the world need a solution to inflation? Is it a problem that needs fixing in the first place? Would a currency with a fixed supply be the answer? The price of everything increasing in dollar terms is a function of more and more money being created. Most everyone recognizes that this is a problem. People seek out different marginal solutions to it; some seek out hedges, in the traditional sense, but everyone is largely conditioned to understand that the dollars in their bank account will purchase less and less over time and act accordingly, trying to escape the impact of its decline. That is the problem and everyone finds the best way to deal with the symptoms of it, which is very different from actually solving the problem. It is the distinction between bitcoin being a hedge to inflation and being the permanent solution to it, such that inflation as a problem no longer exists.

Bitcoin permanently eliminates the ability for more money to be created. If the root cause of inflation is the printing of money, the prevention of that mechanism is definitionally the answer or the solution to the problem. The entire world needs a form of money that cannot be printed for the reason that existing forms of money can be easily printed. It is a need, not a want. But needing something does not make it so. While hedges are designed to protect against the risk of future uncertainty, risk itself is never implicitly knowable. The perception of risk in bitcoin and why many believe it to be a hedge to the dollar is tied to uncertainty. To what extent is it possible to know whether, in fact, bitcoin’s supply is really fixed? To what extent is it a risk or an uncertainty?

The skeptics, or even those who might want to know, typically make a few classes of error: believe that determining whether bitcoin has a fixed supply is unknowable, recognize that it is knowable but believe it is unknowable to them, or a third, do not recognize that it is the right question to ask and never consider it. In each instance, it leaves bitcoin in the minds of most who are conscious of it as, at best, a possibility subject to chance. It is however knowable, with a defined surface area and an empirical record. It is possible to discern. The first step is recognizing that the 21 million fixed supply is the fulcrum; the next is forming some conception or framework as to how it is enforced. Without that as an anchor or guidepost, it would be impossible to tell what is up or down, north or south, in a sea of noise. No one could reasonably evaluate whether bitcoin has fundamental value or how anything, significant or not, impacts bitcoin without one and then the other. Or implicitly, whether bitcoin is a risk or a hedge or the solution to inflation.

Counterparty failures, the Fed printing money, the Fed reducing the supply of money, inflation, the “price” of bitcoin going up, the “price” of bitcoin going down, a Senator from Boston, etc. How could anyone reasonably determine what is relevant, or not, in the absence of a defined reference point to check all assumptions against and amid changing information. It is akin to a person lost in the woods or at sea, with no compass to navigate and no sun or north star to guide them. Totally hopeless and at a loss. There’s a very small chance you might get lucky, but it’s not a winning strategy. Finding the answers is not obvious or easy; it requires effort and intentionality. But with that knowledge, each person becomes armed to survive all weathers–to evaluate every change in information, to consider each event and to decide how to react. It puts every person in control of their own destiny in a way that is otherwise not possible or practical.

Purchasing Power of Bitcoin (Log Scale, 2011-2022)

There is also no way around it. Bitcoin adoption occurs as knowledge distributes, not as individuals make reactive and uninformed speculative decisions. Bitcoin can’t be a “flight to safety,” as the term is often used by the financial investing community in a broad-based way, if the world does not understand it. That is the same reason why it can’t credibly be a hedge. Maybe a gamble, but not a hedge to risk. Bitcoin is not fundamentally a vehicle to offset dollar inflation or to make more dollars, even if some people use it this way.

Bitcoin is a currency with a fixed supply capable of facilitating day-to-day commerce on a direct and global basis. It is competing with the dollar. If bitcoin credibly enforces its fixed supply, it is the solution to the dollar and replaces the dollar. If it cannot, it will not and has no fundamental value. The outcome is binary and the ability for bitcoin to enforce its fixed supply is independent from the dollar. What is certain is that the Fed will create trillions upon trillions of dollars from this point forward and that is a problem. Not knowing or not having done the work does not make bitcoin uncertain.

Risk exists on a spectrum. Uncertainty to some extent is unavoidable. In high finance, there is talk of a risk-free rate. In a financial sense, nothing is actually risk-free. Certainly not government bonds and definitely not the dollar. Bitcoin being a knowable equation is entirely consistent with the acceptance that nothing is without risk. It does not mean that everyone will come to the same conclusion or that degrees of understanding do not vary. A base level of understanding typically forms through a combination of primary education and real-world lived experiences, but it can only harden by having specifically observed and experienced bitcoin working first hand, without fail and amid the chaos of a volatile world, which is really only possible as a function of time.

Bitcoin working is enforcing its fixed supply, on a trustless basis, processing transactions without permissions and necessarily without any central coordination. Each person that figures this out adopts bitcoin as a standard of value. It becomes the least uncertain good in the market. In a world where nothing is certain, it is death, taxes and 21 million bitcoin. There is no silver bullet to understanding bitcoin or a defined end point to learning; that is what makes it difficult. Understanding bitcoin is detached from any single world event or series of events. Instead, it requires a body of work. The mistake is not beginning the journey for fear of not finding the end point. Primed with knowledge, bitcoin is not a hedge to inflation; it is the solution to it. Without prior understanding, bitcoin can practically be neither.

Gradually, Then Suddenly (#18). Fin.

Views presented are expressly my own and not those of Unchained Capital. Thanks to Will Cole, Michael Goldstein, Phil Geiger and Marty Bent for reviewing and for providing valuable feedback.