Has anyone you respect ever told you that bitcoin doesn’t make any sense? Maybe you’ve seen the price of bitcoin rise exponentially and then seen it crash. You write it off, believe your friend was right, don’t hear about it for a while and think bitcoin must have died. But then you wake up a few years later, bitcoin hasn’t died and somehow its value is a lot higher again. And you start thinking maybe your skeptical friend wasn’t right?

The list of bitcoin skeptics is long and distinguished (see here), but the noise contributes directly to the antifragile nature of bitcoin. People that store wealth in bitcoin are forced to think through first principles in order to understand characteristics of bitcoin which otherwise seem, on the surface, to contradict an establishment view of money, which ultimately hardens convictions. Bitcoin volatility is one of these oft-criticized characteristics. A common refrain among skeptics, including central bankers, is that bitcoin is too volatile to be a store of value, medium of exchange or unit of account. Given its volatility, why would anyone hold bitcoin as a savings mechanism? And, how could bitcoin be effective as a transactional currency for payments if its value could reasonably drop tomorrow?

The principal use case for bitcoin today is not as a payments rail but instead as a store of value, and the time horizon for those that store wealth in bitcoin is not a day, week, quarter or even a year. Bitcoin is a long-term savings mechanism and stability in the value of bitcoin will only be realized over time as mass adoption occurs. In the interim, volatility is the natural function of price discovery as bitcoin advances down the path of its monetization event and toward full adoption. Separately, bitcoin does not exist in a vacuum; most individuals or businesses are not singularly exposed to bitcoin and exposure to multiple assets, like any portfolio, mutes volatility of any single asset.

Not Volatile ≠ Store of Value

It is fair to say that volatility and store of value are often confused as mutually exclusive. However, they most certainly are not. If an asset is volatile, it does not mean that asset will be an ineffective store of value. The opposite is also true; if an asset is not volatile, it will not necessarily be an effective store of value. The dollar is a prime example: not volatile (today at least), bad store of value.

“Volatile things are not necessarily risky, and the reverse is also true.”

Nassim Taleb (Skin in the Game)

The Fed has been highly effective in very slowly devaluing the dollar, but always remember, gradually, then suddenly. And, not volatile ≠ store of value. This is a critical mental block that many people experience when thinking about bitcoin as a currency, and it is largely a function of time horizon. While central bankers all over the world point to bitcoin as a poor store of value and not functional as a currency because of volatility, they think in days, weeks, months and quarters while the rest of us plan for the long-term: years, decades and generations.

Despite the logical explanations, volatility is one area that particularly confounds the experts. Bank of England Governor, Mark Carney recently commented that bitcoin “has pretty much failed thus far on […] the traditional aspects of money. It is not a store of value because it is all over the map. Nobody uses it as a medium of exchange,” (see here). The European Central Bank (ECB) has also mused on Twitter that bitcoin is “not a currency”, noting that it is “very volatile” while at the same time reassuring everyone that it can “create” money to buy assets, the very function by which its currency actually loses value and why it’s a poor store of value.

The lack of self-awareness is not lost on anyone here but Mark Carney and the ECB are not alone. From former Fed Chairs, Bernanke and Yellen, to current Treasury Secretary Mnuchin to the President himself. All have, at times, trumpeted the idea that bitcoin is flawed as a currency (or as a store of value) because of its volatility. None seem to fully appreciate, or at least admit, that bitcoin is a direct response to the systemic problem of governments creating money via central banks or that bitcoin volatility is a necessary and healthy function of price discovery.

But luckily for all of us, bitcoin is not too volatile to be a currency and often the experts are not experts at all. Setting logic aside, the empirical evidence shows that bitcoin has proven to be an exceptional store of value over any extended time horizon despite its volatility. So how could an asset such as bitcoin be both highly volatile and an effective store of value?

Bitcoin Value Function Revisited

Consider why there is fundamental demand for bitcoin and why bitcoin is naturally volatile. Bitcoin is valuable because it has a fixed supply and it is also volatile for the same reason. The fundamental demand driver for bitcoin is in its scarcity. To revisit bitcoin’s value function from a previous edition, decentralization and censorship-resistance reinforce the credibility of bitcoin’s scarcity (and fixed supply schedule) which is the basis of bitcoin’s store of value property:

While demand is increasing by orders of magnitude, there is no supply response because bitcoin’s supply schedule is fixed. The disparity in the rate of increase in demand (variable) vs. supply (fixed) combined with imperfect knowledge amongst market participants causes volatility as a function of price discovery. As Nassim Taleb writes in The Black Swan of Cairo: “Variation is information. When there is no variation, there is no information.” As bitcoin’s value increases, it communicates information despite the volatility; the variation is the information. Higher value (dependent on variation) causes bitcoin to become relevant to new pools of capital and new entrants which then stokes an adoption wave.

Adoption Waves & Volatility

Knowledge distribution and infrastructure fuel adoption waves and vice versa. It is a virtuous feedback loop and a function of both time and value. As value rises, bitcoin captures the attention and mindshare of a much wider audience of potential adopters, which then begin to learn about the fundamentals of bitcoin. Similarly, an appreciating asset base attracts additional capital not only as a store of wealth but also to build incremental infrastructure (e.g. more on-ramps & off-ramps, custody solutions, payments layers, hardware, mining, etc.). Developing an understanding of bitcoin is a slow process, as is building infrastructure, but both fuel adoption which then further distributes knowledge and justifies additional infrastructure.

Knowledge → Infrastructure → Adoption → Value → Knowledge → Infrastructure

Today, bitcoin is still nascent and current adoption likely represents <1% of terminal adoption. As a billion people adopt bitcoin, new adoption will represent orders of magnitude for any foreseeable future period which will continue to drive significant volatility; however, with each new adoption wave, the value of bitcoin will also reset higher because of higher base demand. Bitcoin volatility will only decline as the holder base reaches maturity and as the rate of new adoption stabilizes. Said another way, for a billion people to be using bitcoin, adoption will have had to increase by ~20x, but the subsequent 100 million adopters will only represent an additional 10% of the base. All while the supply of bitcoin remains on a fixed schedule. So long as adoption represents orders of magnitude, volatility is unavoidable, but on that path, volatility will naturally and gradually decline.

As Vijay Boyapati explained on Stephan Livera’s podcast, “establishment economists deride the fact that bitcoin is volatile, as if you can go from something that didn’t exist to a stable form of money overnight; it’s completely ludicrous.” What happens between adoption waves is the natural function of price discovery as the market converges on a new equilibrium, which is never static. In bitcoin hype cycles, the rise, fall, stabilization and rise again is almost rhythmic. It is also naturally explained by speculative fear, followed by accumulation of fundamental knowledge and the addition of incremental infrastructure. Rome wasn’t built in a day; in bitcoin, volatility and price discovery are core to the process.

Historical Adoption Wave

For a more tangible explanation of the relationship between volatility and value, it is helpful to think about the most recent adoption wave from the end of 2016 to present (2019).

While adoption can never really be quantified, a rough but fair estimate would be that bitcoin adoption increased from ~5 million people to ~60 million (an increase in demand of ~12 times) from 2016 to present, yet the supply of bitcoin only increased by approximately 10% over the same period. And naturally, the information and capital possessed by market participants varies significantly. As a massive adoption wave occurred, it was met by bitcoin’s fixed supply schedule. What would one expect to happen when demand increases by an order of magnitude but supply only increases by 10%? And what would happen if the knowledge and capital of the new entrants naturally varies greatly?

The very logical end result is higher volatility and a higher terminal value, if even a small percentage of new entrants convert to long-term holders (which is exactly what happened). New adopters who initially purchased bitcoin in its astronomical rise, slowly accumulate knowledge and convert to long-term holders, stabilizing base demand at a far higher terminal value compared to the prior adoption cycle.

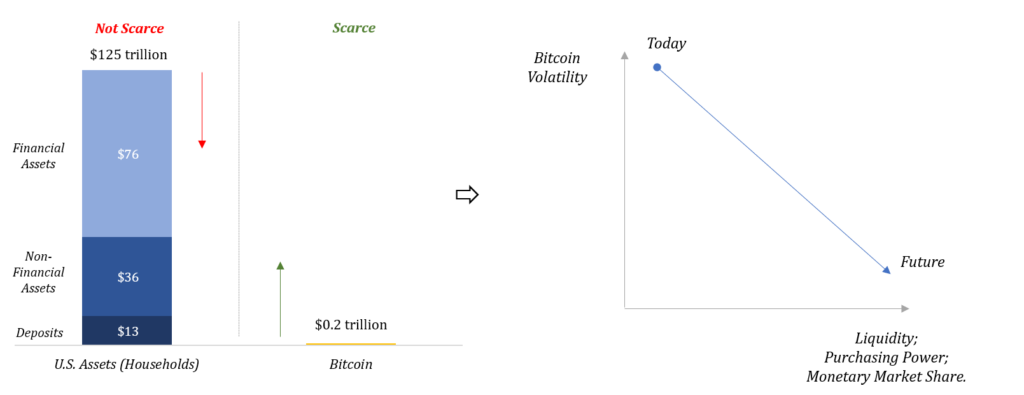

Because bitcoin is nascent, the aggregate wealth stored in bitcoin on a relative basis is still very small (~$200 billion) which allows for the rate of change between marginal buyers and sellers (price discovery) to represent a significant percentage of the base demand (volatility). As base demand increases, the rate of change will begin to represent a smaller and smaller percentage of the base, reducing volatility over time and only after several more adoption cycles.

Managing Volatility

If we can accept that bitcoin volatility is both natural and healthy, why doesn’t current volatility prevent the adoption required to transition bitcoin to a stable form of money? Very simply: diversification, portfolio allocation theory and time horizon. There exists a global network (bitcoin) through which you can transfer value over a communication channel to anyone in the world, and it is currently valued, in total, at less than $200 billion. Facebook alone, on the other hand, is worth in excess of $500 billion. For further frame of reference, U.S. household assets are estimated to be valued at $125 trillion (see here, page 138).

In a theoretical world, bitcoin volatility would be an issue if it existed in a vacuum. In the real world, it doesn’t. Diversification comes in the form of real productive assets as well as other monetary and financial assets, which mutes the impact of bitcoin’s present volatility. Separately, information asymmetry exists and those that understand bitcoin also understand that, in time, the cavalry is coming. These concepts are obvious to those that have exposure to bitcoin and actively account for its volatility in short and long-term planning, but it’s apparently less obvious to the skeptics, who struggle to grasp that bitcoin adoption is not an all or nothing proposition.

While bitcoin will continue to steal share in the global competition for store of value because of its superior monetary properties, the function of an economy is to accumulate capital that actually makes our lives better, not money. Money is merely the economic good that allows for coordination to accumulate that capital. Because bitcoin is a fundamentally better form of money, it will gain purchasing power relative to inferior monetary assets (and monetary substitutes) and increasingly take market share in the economic coordination function, despite being less functional as a transactional currency today.

Bitcoin will also likely induce the de-financialization of the global economy, but it will neither eliminate financial assets nor real assets. During its monetization, these assets will continue to represent the diversification which will mute the impact of bitcoin’s day-to-day volatility. See example here which highlights the risk/return of a 1% bitcoin + 99% dollar portfolio compared to gold, U.S. treasuries and the S&P 500 (@100trillionUSD). Also see The Case for a Small Allocation to Bitcoin by Xapo CEO Wences Casares. Both provide a look through into how volatility and risk can be managed should bitcoin experience a significant drawdown or even fail (which is still a possibility).

While failure is a possibility and significant drawdowns are an inevitability, each day that bitcoin doesn’t fail, its survival becomes more and more likely (Lindy Effect). And over time, as bitcoin’s value and liquidity increase due to its fundamental strengths, its purchasing power will also increase in terms of real goods, but as its purchasing power represents a larger and larger share of the economy, its volatility relative to other assets will proportionally decrease.

The End Game

Bitcoin will become a transactional currency over time but in the interim, it would be far more logical to spend a depreciating asset (dollars, euro, yen, gold) and save an appreciating asset (bitcoin). Establishment economists and central bankers really struggle with this one; but I digress. On bitcoin’s path to full monetization, store of value must come as a logical first order and bitcoin has proven to be an incredible store of value despite its volatility. As adoption matures, volatility will naturally fall, and bitcoin will increasingly become a medium of direct exchange.

Consider the person or business that would demand bitcoin in direct exchange for goods and services. This person or business collectively represent those that have first determined that bitcoin will hold its value over a particular time horizon. If one did not believe in the fundamental demand case for bitcoin as a store of value, why would they trade real-world goods and services in return? Bitcoin will transition to a transactional currency only as its liquidity gradually shifts from other monetary asset to goods and services which will occur along the path to mass adoption. It will not be a flash cut or a binary process. On a more standard path, adoption fuels infrastructure and infrastructure fuels adoption. Transactional infrastructure is already being built but more material investment will only be prioritized as a sufficient number of individuals first adopt bitcoin as a store of wealth.

Ultimately, bitcoin’s lack of a price stability mandate and fixed supply will continue to result in near-term volatility but will drive long-term price stability. It is the literal opposite model pursued by Mark Carney of the BOE, the ECB (and its twitter account), the Federal Reserve and the Bank of Japan. And, it is why bitcoin is antifragile; there are no bailouts and it’s a market devoid of moral hazard, which drives maximum accountability and long-term efficiency. Central banks manage currencies to mute short-term volatility, which creates the instability that leads to long-term volatility. Volatility in bitcoin is the natural function of monetary adoption and this volatility ultimately strengthens the resilience of the bitcoin network, driving long-term stability. Variation is information.

Nassim Taleb & Mark Blyth (Black Swan of Cairo)

“Complex systems that have artificially suppressed volatility tend to become extremely fragile,

while at the same time exhibiting no visible risks.”“This is one of life’s packages: there is no freedom without noise

—and no stability without volatility.”

Ben Bernanke, Chairman of the Federal Reserve (during the Great Financial Crisis)

“The Federal Reserve is not currently forecasting a recession.” – January 10, 2008

“The risk that the economy has entered a substantial downturn appears to have diminished

over the past month or so.” – June 9, 2008

Next week: Bitcoin does not consume too much energy.

Views are expressly my own and not those of Unchained Capital or my colleagues. Thanks to Will Cole, Phil Geiger, Adam Tzagournis and Ethan Packard who have reviewed past and present releases of Gradually, Then Suddenly and provided valuable feedback.