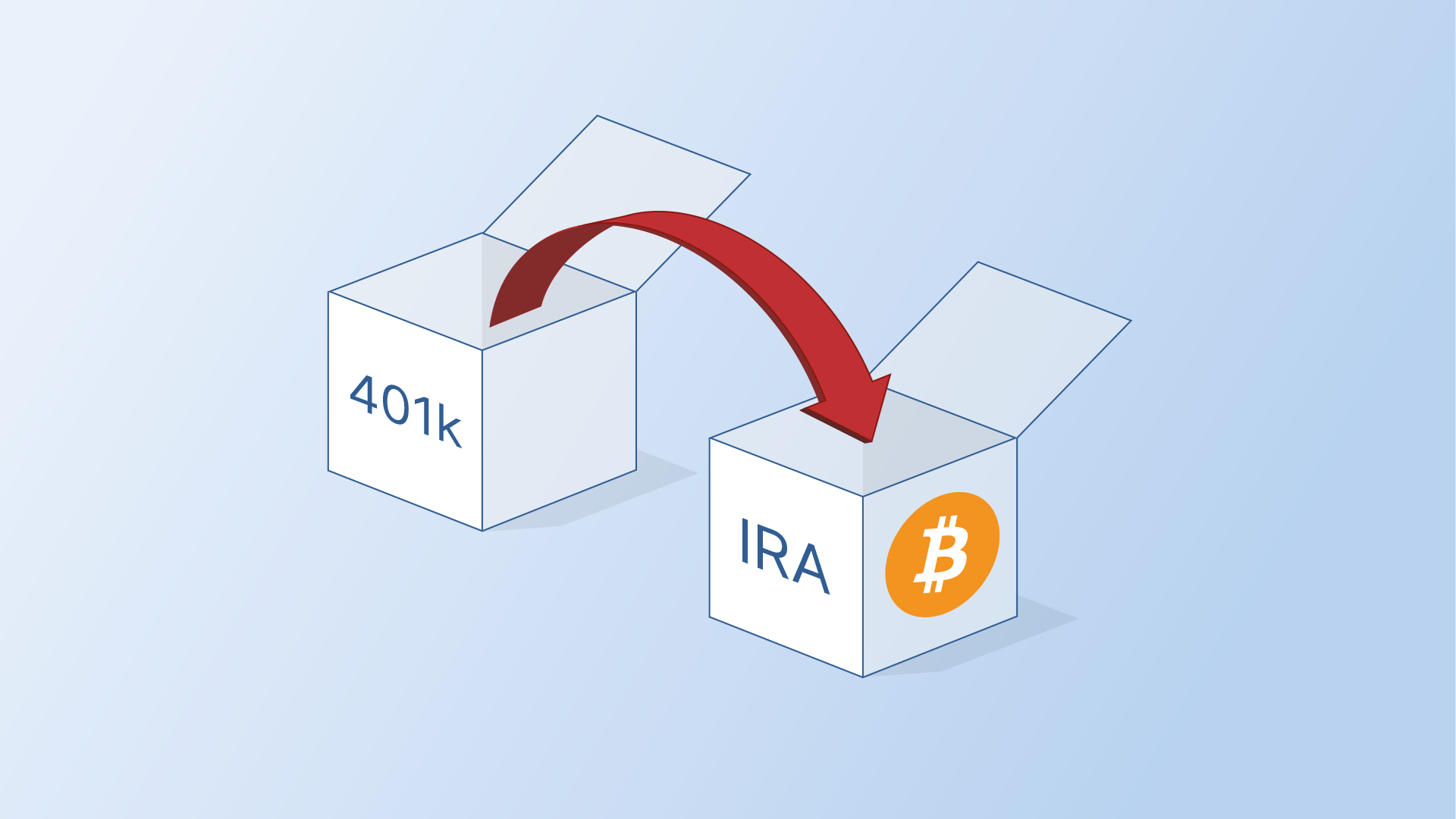

The most common way to fund a bitcoin IRA is by a rollover from an existing retirement plan, often from a former employer. If you’re considering rolling over an employer retirement plan like a 401k into a bitcoin IRA, you should first educate yourself on the tax considerations as well as the mechanics of the rollover.

Tax considerations

Generally not a taxable event, but there are exceptions

Rolling over retirement funds from an external IRA or employer plan (any references to an employer plan in this article mean a 401(k), 403(b), 457, TSP, or defined benefit plan) into a bitcoin IRA is generally not a taxable event. Any non-Roth funds from an IRA or employer plan can be rolled into a bitcoin Traditional IRA tax-free, and any Roth funds from a Roth IRA or employer plan can be rolled into a bitcoin Roth IRA tax-free.

There is a taxable event if non-Roth funds are rolled into a Roth IRA. In that case, the full amount of the rollover is subject to income tax—although it is exempt from the 10% penalty usually imposed on early retirement distributions. The advantage to doing a Roth conversion in this way is that the underlying bitcoin becomes tax-free when withdrawn to be spent in retirement.

SIMPLE IRAs must exist for two years

Another exception to consider relates to SIMPLE IRAs. A SIMPLE IRA must have been in existence for at least two years before it can be rolled into a bitcoin IRA like the Unchained IRA (or any other type of IRA for that matter).

Indirect vs. direct rollovers: only one rollover per year?

You may have heard about a rule stating that only one rollover per year is allowed. Many clients don’t realize that this rule only applies to indirect rollovers, which are rollovers where the client takes actual possession of the funds during the rollover process. Rollovers where funds are transferred directly from one retirement account provider to another are direct rollovers exempt from this rule. There is no limit to the number of direct rollovers which may be done per year.

For a complete look at the different types of retirement plans and where they can be rolled, as well as their stipulations, see this handy chart straight from the IRS. As mentioned above, any footnotes in that chart referencing a one per year limitation relate to indirect rollovers only.

Rollover mechanics

Transfer funds through a direct rollover

To avoid the issuance of a Form 1099R that would trigger potential IRS scrutiny, as well as avoid being limited to one rollover per year, it is best to transfer funds to a bitcoin IRA through a direct rollover. The method for doing a direct rollover depends on whether your funds are coming from an IRA or from an employer plan.

Funds coming from an employer plan

If your funds are coming from an employer plan, after your Unchained IRA is fully set up, you will need to reach out to your plan administrator to request a check be made out directly to your Unchained IRA. Unchained will provide instructions on exactly how the check should be made out when the appropriate time comes.

Funds coming from another IRA

If your funds are coming from another IRA, you will complete a transfer authorization form with that other IRA’s account information during your Unchained onboarding process. That form will authorize Unchained’s banking partner to reach out directly to your prior IRA provider to arrange a direct wire of funds between the IRAs.

A partner for your bitcoin IRA journey

Whether your funds are coming from a 401k or IRA rollover, or you just want to start an annual bitcoin stack, Unchained is here to help every step of the way as your lifelong bitcoin financial services partner. In fact, our Unchained IRA lets you save bitcoin on a tax-advantaged basis while holding your own keys with multisig, and you can learn more in our webinar below.

This article is provided for educational purposes only, and cannot be relied upon as tax advice. Unchained makes no representations regarding the tax consequences of any structure described herein, and all such questions should be directed to an attorney or CPA of your choice.

.png)

.png)